Angel investor Mr Dusan Stojanovic of True Global Ventures (TGV) continues to be our guide in painting the fast-tracked fintech (financial technology) development in Asia, and in relation to the Nordics, part two.

In part one (June 2017) Dusan explained the strategy for his worldwide fintech investment vehicle (focusing solely on B2B fintech investment) and his choice to settle down in Singapore to get things going for real also in Asia; expressed enthusiasm over Singapore’s promising fintech development and its strong support to the ecosystem; and highlighted the opportunity to combine Singapore with Hong Kong for Series B funding. He also predicted that 2017 would be the year when fintech start-ups have to go from Proof of Concept to integration and going live.

What True Global Ventures do within fintech is to assist B2B fintech start-ups at a very early stage and also offer collaboration between the different brands within their investment portfolio.

They have also held ‘Disruption in Banking and Insurance’ events, including in Singapore and Stockholm, with appraised panels on cooperation between financial institutions and start-ups, showcasing growth stage fintech start-ups, identifying future trends and help bringing the industry together.

In November 2016 the Swedish government introduced the Swedish fintech success to Southeast Asia by attending the Singapore Fintech Festival and bringing a business delegation from Sweden.

Building fintech bridges for growth

And while Sweden and Singapore may be in dialogue about entering into official fintech collaboration, Denmark has recently beaten Sweden, with no less than two collaborations inked on paper: between Copenhagen Fintech and Singapore Fintech Association and also between regulators MAS and the Danish Financial Supervisory Authority (Danish FSA). The latter aims to help fintech companies in the two countries expand into each other’s markets, and also to facilitate exchange of regulations information.

In addition, the cooperation agreement framework will enable regulators to share information about financial services innovations, reduce barriers to entry in new jurisdictions and further encourage innovation in Singapore and Denmark.

As for Sweden and Singapore Dusan also believes in stronger bilateral connections to come.

“Singapore and Sweden have many things in common by being open economies – which I believe, looking at the macro economy, is very important in today’s world. New deals between countries that there were not so important 1.5 years ago, is much more important today. I feel that there is there is tremendous amount of things that can be done; in particular within B2B fintech. I think we in Sweden have much better entrepreneurs. A strong entrepreneurship is not being built in a day, even if a government and money wants to do that. But what Singapore is catching up on is the regulatory in that they built an infrastructure, where they, at least regarding the finance inspection part, are well ahead of Sweden! Our central bank in Sweden is probably ahead of Singaporean regarding block chain and Bitcoin etc.”

“No one is best at everything; one is good at some things and less good at others, and in those exchanges many things can evolve. And my goal is of course to have many Swedish companies in Singapore and vice versa, in addition to what I am doing personally. And I think we should bring in India as well – this is the really large market, while we are after all quite small markets. But here in Singapore you have many Indians and we have a fair amount of good entrepreneurs from India also in Sweden even if they are not mentioned much in media. But they are there and if we can bring them on board on this bridge it could turn into something really interesting. India is really opening up now!”

“Once we get those new bridges together we can start talking real growth and not only B2B fintech growth but real growth can make also the entire economy to work. That’s the future – and to act very fast in these economies. Singapore is very open for business, so are India and Sweden. one only needs to wrap it up.”

Cashless societies

Cashless societies

Dusan Stojanovic visited Mumbai earlier this year and says that it was probably the most interesting week he has had in six years.

“We are seeing the demonetisation by the Indian government that is moving ahead incredibly fast, partly when it comes to eliminating cash from the system, which is absolutely the most important thing to get those unbanked banked, and to get some kind of data point on them so that on sees how much money they have in some kind of transaction flow. That is when the banker suddenly takes an interest in them and opens an account for them. If everything is cash one does not even know if it’s an interesting customer or not!”

India had by June 2017 scrapped 86 per cent of its banknotes.

“At the same time you have the other problem that the countryside is not even connected, but the telecom companies are working on that a lot in parallel,” he adds.

Dusan states that the fintech focus here in Asia is on payments: “That’s the most prioritized area. India and Singapore wants to become cashless societies.”

In Sweden cash transactions made up barely 2% of the value of all payments in 2015.

“It is incredibly interesting for these countries. They do analysis on their competitive advantages as a country in the future.”

If you are good at this payment section and come from Sweden I believe there are enormous opportunities in Singapore, India, Indonesia, Thailand, Malaysia, Australia and Hong Kong – those countries have said that it’s very important for their economy; if they can get it to work their GDP will also grow, simply. And that is an infrastructure investment. And after that we will have the same ecosystem that has been developed in Sweden.”

Digital payments and loans

Significantly, the telecoms also have a key role to play and where there is money to be made.

“The real fintech revolution, as far as I can see in Southeast Asia, is coming from the telecom companies. Partly because they control people’s connectivity but also that they have e-wallets and m-wallets and can digitize the usage and purchases. It is enough to open up an account at certain telecoms to use for certain daily needs and also have the connectivity. So there you have it.”

One of TGV’s start-ups, Go Swiff (headquartered in Singapore and with operations in more than 20 countries around the world), is tapping into this, helping to meet the growing demand for digital payments in both emerging and developing markets – boosting financial inclusion and providing a safer, faster and more cost-efficient means of payment.

“We’re doing an implementation in Indonesia with Indosat, where they get both an m and e-wallet solution. We know that China moved very fast with development, now the question is how fast will things happen here in Southeast Asia?”

Sceptics thought: “Things move so slowly that nothing will ever happen. But boy what fools we were, because in India things are progressing very fast now and are then being noticed by the other countries, like: If things can happen there would it not work in SEA and in countries like Indonesia, which is the second largest market in the region?”

Having staked on Indonesia Go Swiff believes this country will follow suit.

“To all of a sudden equip the stalls selling vegetables on the markets in India with Go Swiff etc. and replace the barter trade in India seems like a completely crazy! But that’s what is happening in India today! It is definitely a shift from how you used to do things previously. Most people are actually for this, because those who will lose out are the corrupt ones and those who have had access to a lot of contacts etc.”

Now, as an ordinary person here I can feel: ‘I’m actually part of the system, and actually also part of the bank system. Maybe I’ll also be able to get a loan for my business, something I previously only could get from friends, family or loan sharks.’

And those who have up to now benefited from micro loan systems could be able to do it even simpler and faster than was previously the case, and get even better market conditions, and where this is no longer seen as donation but completely based on real business terms. They should get a lower interest based on all the data that is there, says Dusan.

“So it’s about computerizing information that enables this. If you have data one can give working capital. And we are doing exactly that in Indonesia. Sometimes your supplier even wants payment in advance. If you have financial service data that this trader do get paid they can stretch a lending hand so that the suppliers can be paid on time.”

Paying the supplier forms the basis for how you can develop a business: “If you can get working capital you can grow your business in other ways, such as using profit. So with data you can give that loan. And who are the neediest? The SMEs, as these cannot get these loans from traditional banks.”

“And if you can solve the finances for small companies in the region that will clearly enable the largest leverage when it comes to GDP growth,” he adds.

“Ant Financial in China is the best fintech example that everyone knows right now. The other example is MSwipe in India.”

Ant Financial operates Alipay, the world’s largest mobile and online payments platform and this business is skyrocketing.

“The traditional banks have not dared to enter there because they have not had data, nor seen how they could collect the money due to lack of data about people, and being so scared they’d suffer credit losses. So what you do is to pre-package this for the banks. You get the data and you know the risk you take. So it is the start-up companies finding these customers. The bank only gives the loan when there is a ready package. One does not try to change the behaviour of the banks but to provide them with the information they are looking for.”

In all this the biggest game changer is mobile connectivity – with enough speed. “I’m using the comparison from 1999 when we still were using dial-up modems. In many countries today we have tons of telephones but the connection is still not good but is improving fast. And for every improved connection and data transfer getting faster, and where broadband is being expanded, these countries will get going incredibly!”

But mass consumer adaption is also depending on the policy making of each country: “The only thing we have seen that works is that it must come from a government, as in the example of India, e.g. that there is a real incentive to do the transactions via digital media, via electronic payments etc. It does not happen by itself in a society.”

“When someone dares to put down the feet in the oligopoly, that all these countries are characterized by, and say that this is not financially sound, that it should cost something to pay with cheques, then the whole infrastructure will get going and that’s what we are now seeing twofold in India.”

“Therefore we are monitoring very carefully what is happening there. And we think that whatever happens in India will also happen in the other countries in SEA within an 18 months perspective.”

Fintech solutions for banking sector under threat

Then, the traditional banking sector is of course also being threatened by disruption – with added pressure due to various services like Ant Financial – and clearly forms a big target for fintech innovations too. Most banks in Southeast Asia are now jumping on the bandwagon, with recently, to give one fresh example, Bangkok Bank (Thailand) starting its InnoHub, and where they have handpicked start-ups from worldwide (including one from Sweden) for an accelerator programme.

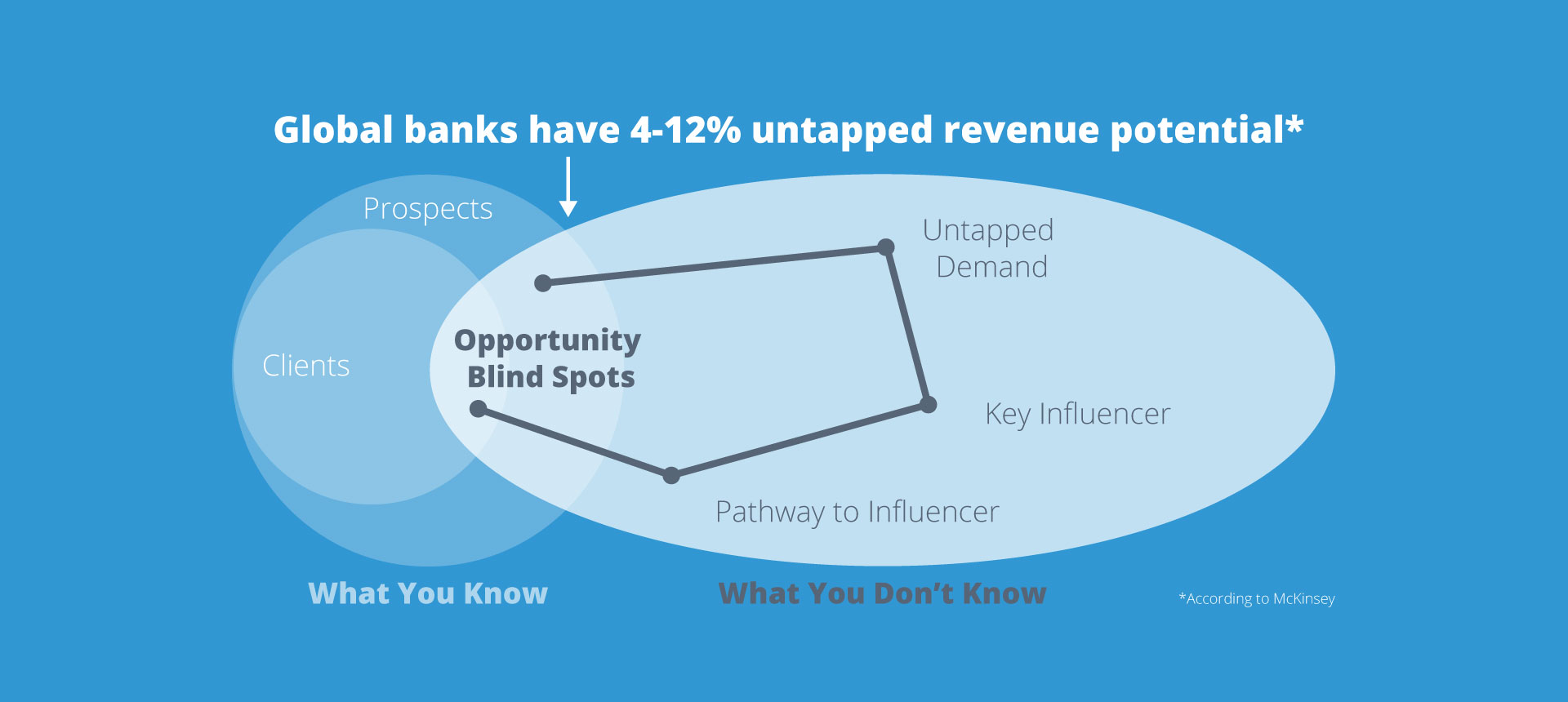

Within fintech innovation for banks the TGV portfolio offers one of their highly relevant Artificial Intelligence (AI) solutions called CustomerMatrix. Global banks and insurance companies, in particular, can use this software to grow revenue and deepen client relationships.

“Having tested on three continents we noticed that this start-up progressed the fastest here in Asia, where we today have offices in both Hong Kong and Singapore, from having had nothing 18 months ago, with 850 per cent registered growth!”

“The basic thing that this company solves that is so tremendously interesting is this: A bank is always interested in new business on corporate level and what it gives is a super linked-in on corporate level where you know who is who all around the world. And that is data we have built up during three years, so partly it identifies a possibility for the bank to do more business.”

“And you have the same thing at the private banking side: is there a customer as co-owner of companies etc.? Can the bank help that customer in ten different ways in real time? So the bank gets the function it had back in the 1800s where it was not about lending money but to identify and create opportunities for the customer to also do business. So that is what has been lost by closing bank offices is the relations – and that is why Handelsbanken keep their offices in order to get that contact that one wants with the customers. AI gives is an incredible amount of data so that when one comes into a customer meeting one is so prepared that one can offer extra business what one was not able to previously without physical contact. So actually we return to the way that banking started – with the assistance of data.”

As for the larger threat to the traditional banking sector Dusan’s take is as follows.

“If you did not have the external threat from these financials things could end up just protecting status quo. But since the outside threat is out there and grabbing market shares they are on their way of losing business. So this threat is absolutely real, especially in the P2P field with its colossal growth. So, of course, the traditional sector wants to defend their business as much as possible and the least changes they have to do the better! But is the outside threat there? Yes! Are decision makers/top management leaving banks for start-ups? Indeed they are!”

“When you see the threat that someone is taking your market share and you are losing your best managers, well then you get scared! And when banks are afraid, you know this is a sweet spot, because then you know they will change.”

“So, right now fintech is winning the fight for talent because you cannot scale these companies if you cannot find the talent. And that is why the partnership turns out to be good, as it is partly based on being afraid.”

Dusan himself bears witness to many bankers entering start-ups. “The bridge is in what I call Fintech 2.0, where the innovation is right there between the banks and the start-ups. And right now most often the start-ups have the strongest product ideas and technology but often lack banking expertise. And there they can still make use of bankers coming over to them explaining the details of how a bank really works.”

And regardless of APIs (enables fintech firms to make use of bank data) open or not TGV are “fighting hard and closing deals”.

“And why is that? There are those on a level within the banks here that are hungry on a completely different level to those in the U.S and in Europe and want to change! You can reach out to the decision-maker very fast. There is leap-frogging!”

“What they lack in technique they have in their Iron will to do things. And compensates well, in such a comparison, so even if we have tons of open APIs in Sweden you do not have faster cycles for fintech companies there just because of that and technically ready to adopt it.”

Here they can also feel for real the external threat more than in the west.

“You have a financial taking market share after market share and country by country, buying itself in or entering organically.”

“So the external threat, combined with having the backbone that exists within the banks to change, is different here. And that makes it more interesting also for start-ups to come here.”

“I am personally interested in investing in and taking all my 1000 relations and have open APIs and just be able to connect my fintech companies, as well as other tech companies. That represents Fintech 3.0 but we are not really there yet, we might reach that in five years’ time.

Read more in Fintech Part One: A true, global business angel: Dusan Stojanovic